The Spring Market is Real - The Price Recovery Isn't

Written by Cody St. Jacques

Is the spring market back? Yes. Are prices bouncing back with it? Not so fast. This spring, activity is heating up across Ontario — more listings, more showings, and more movement from buyers who’ve been waiting on the sidelines. But behind the busy headlines, the reality is more complicated than many sellers expect.

If you've been watching Ontario real estate over the past few years, you know the story. Rates went up, prices came down, and the market has been finding its footing ever since. Now spring is officially here, and everyone wants to know the same thing — is this the year things bounce back?

Here's my honest take: activity is picking up, but don't confuse busy with booming. And there's a new factor in the mix that I don't think enough resale sellers are paying attention to yet.

IN THIS ARTICLE:

What the Numbers are Saying in Guelph Right Now

What’s Coming this Spring

The Mortgage Renewal Wall Nobody Is Talking About

The Builder Wildcard: HST Gone on New Homes

What This Means If You're Thinking of Buying or Selling

The Bottom Line

What the Numbers Are Saying in Guelph Right Now

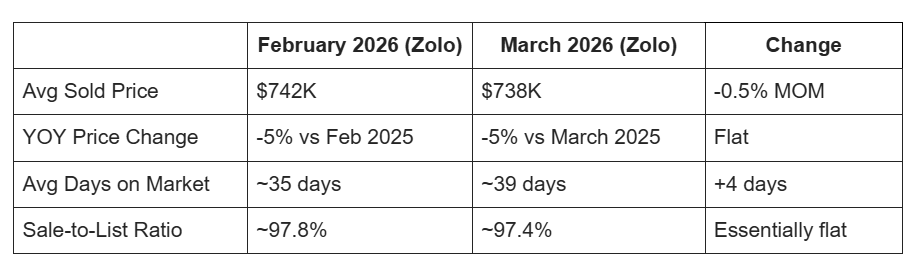

I live and work primarily in the Guelph area, so let me give you the ground-level view. As I'm writing this, the official March 2026 board statistics haven't been published yet — our local board has had some data reporting delays — so the numbers below are pulled from Zolo's MLS data, and I'm using that same source for both months to keep the comparison consistent:

What this tells you: prices have barely moved month-over-month, which might sound like good news — but flat isn't recovery. We're still sitting 5% below where we were a year ago, and homes are taking slightly longer to sell as spring inventory starts to build. The sale-to-list ratio holding near 97–98% tells you the same thing it did in February: when homes are priced right, buyers are still showing up. They're just not overreaching.

What's Coming This Spring

Spring traditionally brings two things: more buyers and more listings. This year, I expect both — but with a twist.

More buyers, yes. Lower rates are bringing people off the sidelines who've been waiting. Pre-approvals are up, buyer inquiries have been climbing since January. With the exception of some tariff-related uncertainty that spooked the market in early 2025, February and March are typically the start of the spring market — and 2026 is shaping up to follow the more predictable seasonal pattern.

But the supply side is the real story. We're going to see a meaningful wave of new listings this spring — and layered on top of that, a significant number of sellers who listed in 2025, didn't get their price, pulled their homes off the market, and are now coming back with renewed hope. That's a double layer of supply hitting at the same time buyer demand returns. When supply and demand both rise together, prices don't necessarily follow.

The Mortgage Renewal Wall Nobody Is Talking About

There's a bigger economic story quietly playing out in the background — and it's going to shape this market for the next couple of years.

Think back to early 2022. That was the last gasp of the ultra-low rate environment from the COVID era — rock-bottom rates, record prices, and buyers locking in 5-year mortgages at numbers we'll probably never see again. Those mortgages are coming up for renewal right now.

For a lot of homeowners, that renewal means a significant jump in their monthly payment. Some will absorb it. Some will be forced to sell. That renewal pressure has contributed to a gradual increase in power of sale activity — not a flood, but a drip — and it's worth watching because distressed sales can create localized price pressure and set the tone in certain segments of the market.

I expect downward pressure on price to continue through at least Q1 2027. After that, most of those renewals will have cycled through, and the market will be operating on a more level playing field. Those who purchase in that environment will have already factored current rates into their decisions — fewer payment shocks, more stable footing going forward. In plain terms: weather the next 12–18 months, and the headwinds start to ease.

The Builder Wildcard: HST Gone on New Homes

Here's the factor I haven't seen enough people talking about yet — and if you're a resale seller in a certain price range, you need to understand what just happened.

On March 25th, Premier Doug Ford announced that the full 13% HST will be removed on new homes valued up to $1 million — effective April 1, 2026 through March 31, 2027. For homes up to $1.5 million, the maximum $130,000 rebate is maintained, then it phases down gradually to roughly $24,000 at the $1.85 million mark.

To put the scale of this into context: new home sales across Ontario fell to approximately 15,000 units in 2025, down from historic annual levels of 65,000 to 85,000. Condominium apartment sales were down 89% from the 10-year average. The preconstruction market has been on life support. This rebate is designed to change that — and I think it will.

Here's my honest take on what that means for Guelph's resale market:

Builders who were already carrying unsold inventory and offering heavy discounts now have a government-backed tailwind worth up to $130,000 baked into every deal. A buyer who was comparing a $750,000 resale townhouse to a $750,000 preconstruction townhouse just had the math completely rewritten. The new build is now materially cheaper — potentially by close to $75,000 — and it comes with a warranty, brand new finishes, and no competition from other buyers on closing day.

I do think this is going to draw buyers into the preconstruction market who otherwise would have been resale buyers. That's good for builders and good for housing supply long-term. But in the near term, it creates a new competitive pressure on resale — especially in the $600,000–$1,000,000 range where the overlap with new construction is highest. Resale sellers in that bracket are now effectively competing against builders who just got a massive pricing advantage handed to them by the government.

That doesn't mean resale can't compete. Character, location, mature neighbourhoods, no construction risk, immediate occupancy — those things matter. But it does mean resale pricing has to be honest about where the market actually is, not where sellers wish it was.

What This Means If You're Thinking of Buying or Selling

If you're selling: pricing right is everything — and that statement just got more urgent. The 97–98% sale-to-list ratio tells you buyers are engaged, but they're doing their homework. They're now doing that homework against a backdrop where new construction just got a lot more attractive. Homes that are overpriced are sitting. Homes priced with the market are moving in about 35–39 days. Don't list at what your neighbour got in 2022. List at what the market actually supports today.

If you're buying: this is one of the better windows in recent memory. You have negotiating room, you have time to do due diligence, and you have a genuine choice between resale and new construction that hasn't existed this clearly in years. If you're open to preconstruction, the math has shifted significantly in your favour — talk to someone who understands both sides of that equation before you decide.

The Bottom Line

Spring 2026 is going to be an active market. More transactions, more listings, more movement. But active doesn't mean prices are going back up — at least not yet. The supply pressure from returning 2025 sellers, mortgage renewal-forced listings, and now a government-backed incentive steering buyers toward new builds is real, and it's going to keep a lid on appreciation in the resale market for the near term.

What I tell my clients: don't wait for the perfect market. Make the decision that makes sense for your life, price it properly, and trust the fundamentals. Guelph is still a strong, desirable city. People aren't moving away — they're just adjusting to a new normal.

And that new normal? It's more complex than it looks. But complexity is where good advice matters most.